The Employee Retention Credit (ERC) is a refundable tax credit for businesses that continued to pay employees while sustaining a full or partial suspension of operations limiting commerce, travel, or group meetings due to COVID-19 and orders from an appropriate governmental authority.

The CARES Act and subsequent acts created ERC because the federal government wanted to provide payroll relief for those employers who kept employees on the payroll during COVID starting March 13, 2020, through September 30, 2021. It is a refund issued by the IRS that allows a church to spend money on whatever they choose or save for the future. It requires complex calculations and is applied for by filing modified payroll tax returns for the period. As a result, each quarter of 2020 and 2021 are analyzed from payroll data to determine the refund amount. Subsequently, a check is issued for each quarter if it is approved.

History

ERC is not new. It was used to support the recovery efforts of employers who experienced losses from Hurricane Katrina in 2005. It was repealed by Congress in 2018 for the purposes of Katrina relief.

Current State of ERC

These acts led to the current ERC.

CARES ACT

ERC was initially enacted as a part of the Coronavirus AID Relief and Economic Security Act (CARES Act) on March 27, 2020, making it retroactive to March 13, 2020. In addition to ERC, the CARES Act also included provisions more familiar to the general public, such as the Paycheck Protection Program Act (PPP) and Economic Injury Disaster Loan (EIDL) loans, Families First Coronavirus Response Act (FFCRA) for sick leave, and more. The CARES Act enacted ERC for quarters in 2020.

Taxpayer Certainty and Disaster Tax Relief Act of 2020 (Relief Act)

The main provision of the Relief Act was to remove the prohibition of getting a PPP loan and not ERC, or vice versa. Enacted December 27, 2020, businesses could now get ERC even if they received one or both PPP loans available with the caveat that PPP loan amounts used for payroll could not be used in the calculations for ERC relief. It also extended ERC into the first two quarters of 2021.

American Rescue Plan Act of 2021 (ARPA)

ARPA was enacted on March 11, 2021, and further expanded ERC to include the last two quarters of 2021.

Infrastructure Investment and Jobs Act (Infrastructure Act)

The Infrastructure Act was enacted on November 15, 2021, and repealed the general availability of relief in the fourth quarter of 2021. It is still available, but only to Recovery Start-up Businesses and not those that were in existence prior to February 15, 2020.

Common questions about ERC

- Are we eligible if we received one or both PPP loans? YES. The misconception that getting a PPP loan precluded getting ERC is founded in the CARES Act, which initially prohibited receiving both ERC and PPP, but the prohibition was repealed in the Taxpayer Certainty and Disaster Tax Relief Act of 2020.

- Our revenues did not go down. Do we qualify? YES. There are two different ways to qualify – either a reduction in revenue or a disruption in operations. Most churches qualify due to a disruption in operations.

- Are there limitations on the size of organizations (number of employees) that can get ERC? NO. However, additional calculations are necessary to determine the extent of qualification and the refund amount. We will require payroll information for all of 2019 in addition to that of 2020 and 2021.

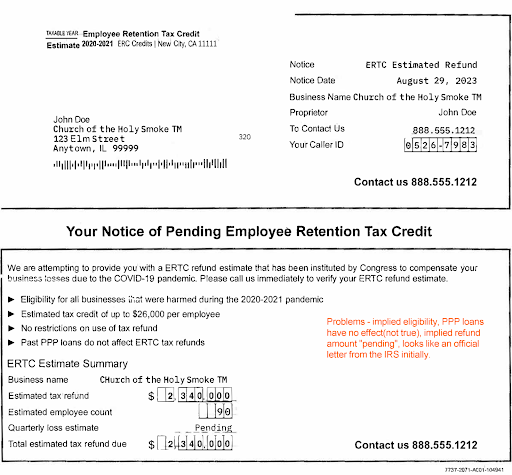

- Is there a time limit in which we need to apply? YES. Do not delay. There is both a time limit and a dollar amount authorized by Congress for refunds. If either is reached, you will not have an opportunity to file. The ability to file for ERC begins to decline quarter by quarter on April 15, 2024 and ends on April 15, 2025.

What do we need to do to apply for ERC refunds?

First, you need to confirm your eligibility with the IRS. The IRS website includes the forms to complete, but you may want to hire a tax professional to navigate the process.

While the ERC application process is complex, it’s absolutely worth the investment to recover funds lost during COVID-19 and does not impact a PPP plan if your church has one. If you’d like help with the ERC process, click here.